Private markets infrastructure: how Motive's wealth tech ecosystem is unlocking access to alternative investments

Introduction

This scene repeats daily across wealth management: an investor wants access to private markets, an advisor opens a 47-page subscription document, compliance flags questions, and weeks pass while nothing moves. The investor interest in the asset declines, the advisor has other things to do which require less admin, and the allocation never happens. Private Markets are attractive from a return’s perspective, they become ugly when you step through the processing complexity.

It is a significant opportunity.. But can advisors place $22 trillion (McKinsey & Company, 2025) of private markets into retail portfolios, using an infrastructure that runs on PDFs, paper documents, signatures and email chains.

Women, Gen Z and Millennials are about to inherit ~$85 trillion (Cerulli Associates, 2024), and they expect Amazon-type buying experiences. The expectation vs experience gap is currently significant. But the opportunity remains once in a generation.

For decades, alternative asset managers have operated in scarcity: scarce capital, scarce deal flow, and distribution concentrated around large institutions. The playbook was simple (raise, deploy, return, repeat) and distribution meant in-person visits to pension funds and endowments, not technology-enabled access for individual investors. The world of fund raising is changing, and the infrastructure needs to keep pace. For an industry managing $22 trillion (McKinsey & Company, 2025) in assets, this is not just an inefficiency wrinkle; it is an existential threat to realize the full potential.

The thesis is direct: the firms who solve the three-sided infrastructure challenge of digitizing asset managers, connecting them to wealth distribution channels, and enabling individual portfolio construction to include private markets, will capture disproportionate value. Doing so requires building what is missing: a comprehensive operating system for private markets that spans connectivity, data infrastructure, intelligence, marketplace technology, execution and processing capabilities (Fink, 2025).

The coordination failure

The Private Markets' distribution challenge is several distinct problems masquerading as one. Asset managers will struggle to service individual investors at scale, wealth platforms lack the plumbing to include illiquid assets in whole portfolios, and individual investors remain locked out by institutional-only structures, advisors do not feel comfortable allocating to private markets because they are still learning how the asset class performs. Each constituency wants access, but the connective tissue is lacking.

Think about it. A private equity fund raising $1 billion from 20 institutional investors manages roughly 20 subscription documents. The same raise from 50,000 individuals at $20,000 each creates 50,000 subscription documents, each with KYC, suitability, and ongoing servicing, and a much higher NIGO (Not InGood Order) rate. Without automation, the operating model breaks. The data problem compounds it. Public markets run on shared identifiers, centralized pricing, and common formats. Private markets do not. A fund's data can live in dozens of formats across as many systems, so every wealth-platform integration becomes bespoke and uneconomic at scale.

Point solutions addressing specific constraints (subscription tools, data aggregators, standalone marketplaces) provide meaningful value, but highly fragmented. The breakthrough comes from connecting these solutions into an integrated infrastructure.

Consumer technology has created a scalable pattern. When Netflix digitized content; it also built recommendation engines, personalization systems, and streaming infrastructure. Spotify delivered playlists, not just a music library. Private markets need the same shift: comprehensive infrastructure that serves all participants and creates compounding network effects across the ecosystem.

The marketplace model

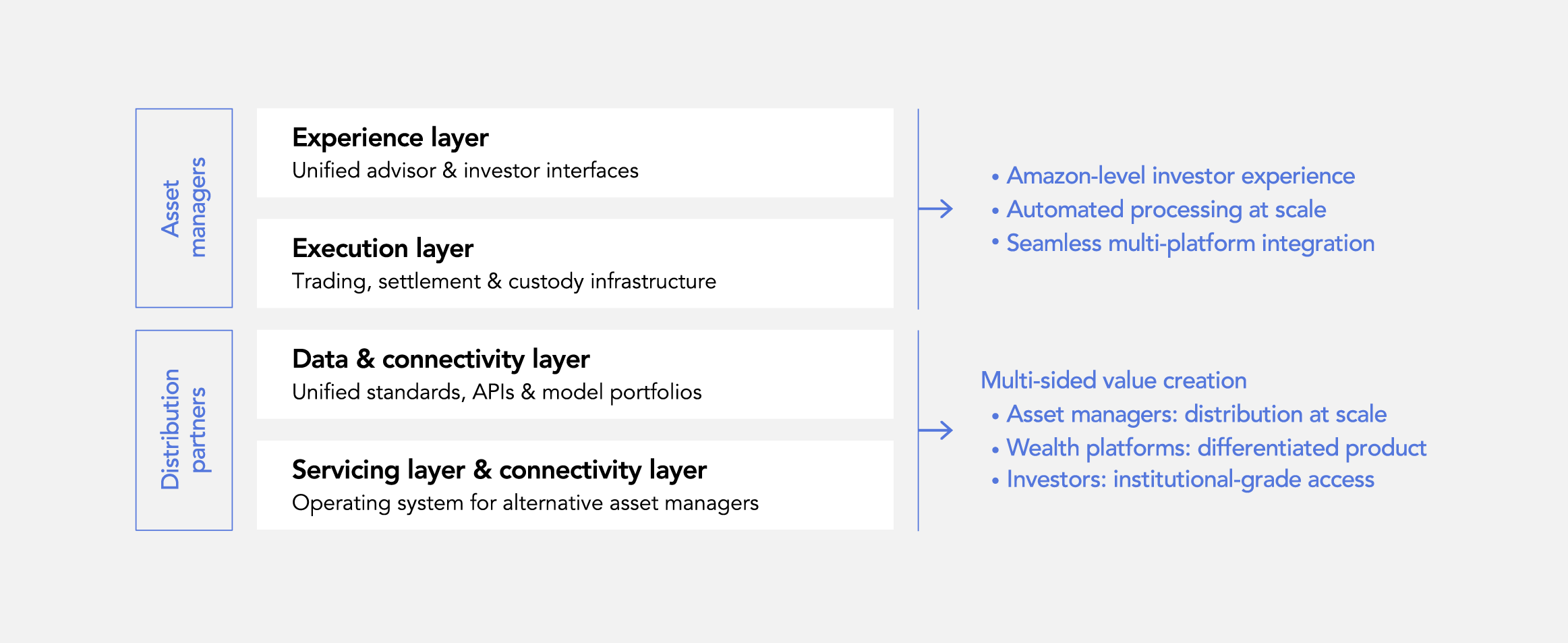

The solution follows a recognizable pattern: build network infrastructure that represents both sides (asset manufacturers and distribution channels), then layer on data intelligence and connectivity. This approach mirrors successful consumer platforms but requires financial services-specific components. The core architecture needs four layers working together:

Servicing layer: Operating systems that digitize alternative asset managers' operations: subscription workflows, fund data standards, investor servicing at scale. This is the fundamental operating system that lets private markets integrate with wealth platforms.

Data and connectivity layer: Unified data standards for private markets, enabling fund information to flow seamlessly between asset managers and wealth platforms (Fink, 2025). Model portfolio platforms that can incorporate illiquid assets. APIs connecting previously siloed systems.

Execution layer: Trading and settlement infrastructure for private market products. Custody solutions. Processing engines that handle the unique mechanics of private markets transactions, the digitization of fund administration and transfer agents.

Experience layer: Digital interfaces for advisors and investors that make private markets as easy to execute as a mutual fund. Portfolio analytics that properly reflect illiquid holdings. Compliance tools embedded in the user experience.

This architecture creates network effects on both sides. Asset managers accelerate scaled distribution. Wealth platforms access differentiated product without bespoke integration and manual intervention. As more participants join, the infrastructure scales gracefully and becomes more valuable to all participants.

Investment implications

Several indicators underpin viable infrastructure plays:

Multi-sided value creation: Does the platform solve problems for both asset managers and distributors? How does the platform solve the cold start challenge? Single-sided solutions face chicken-and-egg problems and limited pricing power.

Standards versus features: Is the company building proprietary standards that create lock-in or features that can be replicated? Data standardization and operating system infrastructure create more defensible moats than user interfaces.

Integration depth: How embedded is the solution in core workflows? Platforms that become systems of record exhibit stronger retention than those solving point problems.

Capital efficiency of growth: What is the marginal cost of adding the next user? True network businesses show improving unit economics at scale, not linear cost structures.

Liquidity readiness: Do all individual investors tolerate illiquidity less than institutions? Lending against private holdings (with real-time valuations, household balance-sheet integration, and strategy-aware underwriting) removes a key barrier without forcing managers to change fund structures. Done well, this turns private markets from a niche allocation into a core portfolio component.

Regulatory trends support this infrastructure build. The SEC's focus on improving individual investor access to private markets creates tailwinds for compliant, scalable infrastructure. Platforms that embed regulatory compliance have structural advantages over those treating it as an afterthought.

Signals and the road ahead

Several signals will indicate infrastructure momentum over the next 24 months:

Transaction volume shifting from traditional channels to digital platforms, with the crossover point marking a critical milestone. Adoption by top alternative managers (how many of the top 50 deploy dedicated wealth infrastructure rather than manual processes). Integration patterns on wealth platforms, showing either broad multi-vendor approaches signaling commoditization or consolidation around few providers signaling winner-take-most dynamics.

Asset managers designing products for digital channels, rather than retrofitting existing structures, signal genuine commitment to the shift. Realized margins at infrastructure providers, either expanding with scale or compressing as technology lowers unit costs. Regulatory clarity on individual access determines the timeline: three years or ten.

Looking forward, the infrastructure will become invisible (Fink, 2025). It becomes the internet or the cell tower, it is just there. Advisors can add private credit, private equity, and real assets to portfolios as easily as they add bonds. Asset managers can distribute through wealth channels the way consumer fintechs originate from user bases. Individuals will be able to borrow against private holdings as easily as against a personal asset.

$85 trillion (Cerulli Associates, 2024) is moving to a new age of investors who expects digital access but institutional-grade returns. The value will accrue to those who built the connective tissue of the system, not just the endpoints.

Motive Partners: building the operating system

Motive Partners portfolio companies are building the infrastructure that makes private markets accessible at scale. The firm's approach mirrors the four-layer architecture: assemble components across servicing, data, execution, and experience, then connect them so the system moves as one.

Servicing layer: Vega (backed by Motive Partners and Apollo) provides the operating system for alternative asset managers by digitizing subscription workflows, standardizing fund data, and managing investor servicing at scale. It handles the operational complexity of moving from 50 institutional LPs to 50,000 individual investors. InvestCloud brings private markets into the managed account via its Private Markets Account (PMA),with its APL platform managing more than $3 trillion in assets across 10million accounts (InvestCloud, 2024). Advisors construct portfolios that blend public and private holdings under unified governance, with compliance tools embedded and portfolio analytics reflecting illiquid positions.

Data and connectivity layer: Daphne establishes the product standards that let fund information flow between managers and technology platforms without bespoke integration. What the CUSIP did for equities, Daphne will provide for private markets: unified identifiers, centralized data formats, and APIs that connect previously siloed systems. BetaNXT automates complex workflows across the investment lifecycle, processing data and enabling straight-through processing for both public and private

assets. Zocks captures investor data at origination.

Execution layer: CoraStone handles execution and settlement for private markets investments. CAIS operates the largest alternative investment platform for independent financial advisors, serving over 2,000 wealth management firms supporting 50,000+ financial advisors (CAIS, 2025). Lyra manages the client services experience while Alchelyst handles fund administration. Together they ensure transactions clear, and portfolios stay current without manual intervention.

Experience layer: InvestCloud's platform serves as the unified interface where advisors see one clean experience from proposal to statement. Vega writes lifecycle events (capital calls, distributions) directly back to InvestCloud's books. Lyra processes servicing requests seamlessly in the background. FNZ and Upvest extend this unified experience across global wealth platforms.

What this unlocks: The same advisor and investor sit down again, but this time the conversation is different. Onboarding and suitability happens in real time, the subscription generates systematically, and the allocation funds in minutes instead of weeks. The investor sees exactly when capital is deployed, how liquidity can be accessed, and how the private markets position sits inside the portfolio. The meeting ends with progress, instead of promises and hope.

The network effects: 50 million investors reached, 150,000 advisors served, 600 distribution partners, 500 asset managers connected, $10 trillion in AUM managed. Private markets democratization is real, but the infrastructure was constrained. That constraint is lifting. The firms that built the connective tissue will capture disproportionate value as the market scales. The firms that waited will be renting someone else's rails.

Download the perspective: Private markets infrastructure: how Motive's wealth tech ecosystem is unlocking access to alternative investments