Challenges and opportunities in capital markets

Challenges and opportunities in capital markets - The innovation imperative

Capital markets are essential to the global financial system, enabling businesses, governments, and investors to raise capital, fund projects and manage risks. However, their interconnectedness, regulatory demands, and complex operational environments often constrain innovation.

Over decades, capital markets have transitioned from manual, intermediary-driven processes to more automated systems. The 1980s and 1990s brought electronic trading and post-trade systems, increasing efficiency. But despite advancements like automation, low latency systems, standardization, straight-through processing (STP), and cloud platforms over the last two decades, progress has been uneven. Key areas such as private markets, fixed income, and post-trade services lag in technological adoption due to legacy systems, regulatory challenges, and fragmented ecosystems.

The barriers to transformation are both structural and cultural. The complexity of global markets makes change operationally risky, as failures in critical processes—like US debt market settlements— could have catastrophic consequences. Regulations typically prioritize stability and careful evaluation of new technologies like blockchain or AI, while market participants often favor short-term stability over long-term strategic innovation.

This thought piece explores how new technologies can achieve a future-ready system to overcome barriers and enable incumbents to embrace change. We will outline key sub-segments that we are actively focusing on, which we believe hold significant potential to drive transformative change in capital markets.

What does this mean for early-stage innovation in capital markets?

For Motive Ventures, choosing the right companies to invest in is driven by our conviction of their right to win: do they have a vision, resources, expertise, track record, and market entry strategy that is fully aligned to the current operating environment to deliver value through transformational change? For new innovators, we believe the following factors can heavily weigh on making sure disruptive technology in capital markets is set up for the highest chance of success.

- Thinking global from day one

Capital markets operate on a global scale, creating opportunities for fintech innovators but also demanding strategic decisions. Early-stage companies must decide whether to build globally scalable solutions or specialize in addressing specific regional and asset class nuances. Compliance and licensing are significant hurdles, often making scalability a challenge. Successful innovators require both a global vision and a phased go-to-market strategy to grow sustainably.- Capital markets operate on a global scale, linking economies and institutions in a massive and intricate web of connected ecosystems. Traditionally, this interconnectedness means operational or technological change tends to involve large scale change management programs, and failure carries the potential for widespread disruption. Early-stage companies must decide whether to build globally scalable solutions or specialize in addressing specific regional and asset class nuances.

- Capital markets require a high level of nuances across asset classes and geographies. In Europe, for example, navigating different capital market unions and exchanges adds significant complexity.

- Lastly, one should understand regulatory impacts: Establishing compliance frameworks and obtaining licenses can be prohibitively expensive for young companies, often making scalability a formidable challenge.

- Navigating a high-complexity ecosystem

The diversity in asset classes, regional regulations, and technological infrastructures makes innovation in capital markets difficult. New innovations and early-stage companies should:- Serve the client without over-customization: Early-stage businesses need to deliver value without falling into the trap of building overly bespoke solutions that hinder deployment and scalability.

- Adopt an open architecture: Innovators must understand how the solution fits within

the ecosystem, and what existing systems it replaces, augments or integrates to. They must create systems that seamlessly connect with multiple stakeholders and existing infrastructure, ensuring their solutions are both compatible and adaptable. If a good solution already exists, don’t replicate it, integrate to it. - Identify the beach head: Early-stage businesses should focus on a specific area of the value chain where there is a clear need, work alongside existing players who are motivated to change and are prepared to invest time and money for success. By emphasizing flexibility, connectivity, and strategic focus, early -stage firms can become indispensable players in the ecosystem.

- Making change a rational decision

Decision-makers in capital markets on the receiving, incumbent, end will prioritize stability and cost-effective improvements over high-risk, large-scale innovation. Early-stage innovators need to find ways to be able to cope with these decision dynamics- Demonstrating incremental value: Instead of proposing wholesale overhauls, innovators should focus on solving specific pain points with measurable outcomes.

- Building trust through working with incumbents: Collaborating with existing players can provide early-stage companies with the momentum and credibility needed to gain market traction.

- Showing the pathway to the end-state solution: Having the necessary subject matter expertise and demonstrated track record of success will help to convince buyers that a strategic solution can be delivered in the long term.

Collaborations between innovators and incumbents leverage the strengths of both, combining market reach and operational knowledge with agility and cutting-edge technology. Together, they can create transformative, high-value solutions for the market

Selected "Innovation imperatives" within capital markets

As discussed, the bar to deliver benefits through innovation in capital markets is and will remain high and therefore building a sustainable business has its challenges. However, we do still see gaps in the market where new technologies will shape the ecosystem and can fundamentally change the way of business going forward.

Electronification: progress in capital markets

Electronic trading is revolutionizing capital markets by automating trading processes and improving price transparency and liquidity across multiple asset classes. Despite advancements in some areas, many markets, such as fixed income, small-cap equities, alternatives, private credit and unlisted equities are in various stages of their electronification journey.

Markets such as fixed income are still heavily reliant on voice-based trading, which reflects the complexity of the products, the commercial incentives of the intermediaries, and the fragmentation of existing systems.

The inefficiencies inherent in this limit liquidity and restrict access to broader market participants. Sophisticated electronic trading solutions are now emerging, designed to address these inefficiencies – with solutions tailored to different needs by asset class and geography and focused on a more diverse set of buyer personas instead of simply institutional appetite.

By automating trading processes, these solutions enhance secondary market liquidity and improve accessibility for participants on a global scale. Additionally, we believe the financialization of emerging markets through these technologies represents a significant opportunity for market integration and growth.

Nevertheless, this industry thus far has been dominated by large E2E platforms, presenting their respective offerings as multi asset / multi geo on both the buy and the sell side covering many aspects of the market. While these players have created the first wave of innovation, we believe a second wave is currently in motion. While the concept of multi-asset, multi-geography solutions still stands, the reality remains fragmented. Why is that the implementation of multi-asset solutions has lagged thus far?

- Complex needs: Buy-side and sell-side users require different workflows depending upon their size, their location and the asset classes they trade.

- Fragmented infrastructure: OMS/EMS platforms have evolved as point solutions, which solve these complex, but do not integrate to a common system architecture, creating a mosaic of disparate systems.

- Decentralized decision-making: Global clients of these solutions tend not to make decisions that consolidate across multiple asset class, allowing decision makers with responsibilities at the trading level to choose the solution that best suits their needs.

- Tight margins: Existing players struggle to reinvest in better technology and services. As a result, service quality and innovation have declined.

- Fragmentation: There is no unified platform that serves multiple jurisdictions or asset types. Each player focuses on specific geographies or asset classes, leading to inefficiencies and dissatisfied customers.

- Limited innovation: Decision-makers within asset servicing often prioritize incremental improvements within their own asset classes rather than embracing transformative solutions.

Several of the incumbent solution providers have followed an acquisition strategy aimed to integrate offerings across asset classes and geographies, but consolidation into a core technology solution has been a challenge. A lack of investments, legacy architectures, and loss of subject matter expertise have limited the incumbents’ ability to deliver the seamless experience that users expect. While this consolidation strategy has the promise of greater investment in innovation, improved responsiveness to customer needs and lower operating costs, the execution strategy has not yet been realized.

Digitisation: innovation in share and fund registry

he asset servicing functions performed by registries, a critical function in capital markets, has seen margins eroded over the years due to intense competition and driven by the challenges the legacy technology that is in operation today. The systems are hard to change and maintain, are built to operate within specific jurisdictions and regulatory frameworks, data is siloed, and manual processes remain commonplace to manage corporate actions. This makes it challenging to drive down operational costs and build contemporary digital experiences for clients.

Notwithstanding this, larger platforms and others have done a commendable job - but the market remains fragmented. Without a common, multi-jurisdictional platform to manage both public as well as private assets, the industry continues to suffer from inefficiencies, subpar services, and stagnation in innovation. But why is the status quo not working?

Therefore, there is an opportunity for a common platform: A single, multi-jurisdictional platform could bring together the core functions of asset servicing including functions like transaction processing and compliance for both public and private assets.

A combined approach would streamline operations, improve service quality, and lower costs. Technologies such as blockchain and cloud native platforms can allow for higher degrees of speed, transparency, security and unification while remaining customer centric.

The financialization of new asset classes: private credit

The emergence of new asset classes like private credit, crypto and carbon credits are reshaping capital markets, offering unique opportunities for both investors and infrastructure providers. Unlike traditional asset classes, these markets lack established market infrastructure. This an advantage - allowing infrastructure to be built from the ground up, tailored to today’s needs and using contemporary technologies. It is also a challenge – the lack of institutional-grade market technology will take time to build and is often under-estimated.

For example, private credit has seen explosive growth as an alternative to traditional fixed income, with institutional investors drawn to its higher yields and tailored structures post financial crisis 2008. Private credit’s global AUM surpassed $1.5 trillion in 2023 and is forecasted to reach $2.8 trillion by 20281. Unlike traditional lending, private credit offers bespoke solutions tailored to borrowers’ needs, including direct lending, mezzanine financing, distressed debt, and asset-backed lending.

However, as the asset class grows, it is casting its net wider through increasing number of distribution channels, wider set of lending lines and targeting a broader set of customers. This explosive growth presents unprecedented opportunities but also demands robust technological frameworks to support and scale the asset class effectively. Technology is fundamental to fueling this expansion increasing connectivity to distribution channels, enabling innovation across asset backed lending lines and enabling private credit to efficiently underwrite, originate and service customers. Key aspects of this are:

- API integration: Streamlining how private credit funds interact with balance sheets, enabling seamless connectivity for distribution partners and accelerating deal flow.

- AI-driven credit agreements: Leveraging AI to digitize and analyze credit agreements, empowering stakeholders with enhanced control, real-time insights, and optimized deployment of capital.

- End-to-end process automation: Digitizing every stage of the credit lifecycle to ensure operational efficiency, faster execution, and reduced costs.

- Data standardization: Establishing a unified framework for valuation, risk assessment, and trading, simplifying syndication and securitization.

- Real-time monitoring: Deploying advanced tools for real-time insights into private credit performance, enabling proactive decision-making.

As private credit providers increasingly tap into consumer “flow” lending, the need for scalable technology becomes paramount. Supporting high-volume, low-value lending requires infrastructure capable of automating processes, minimizing risk, and delivering cost efficiencies. These advancements will not only unlock growth in consumer lending but also drive innovation across all facets of private credit.

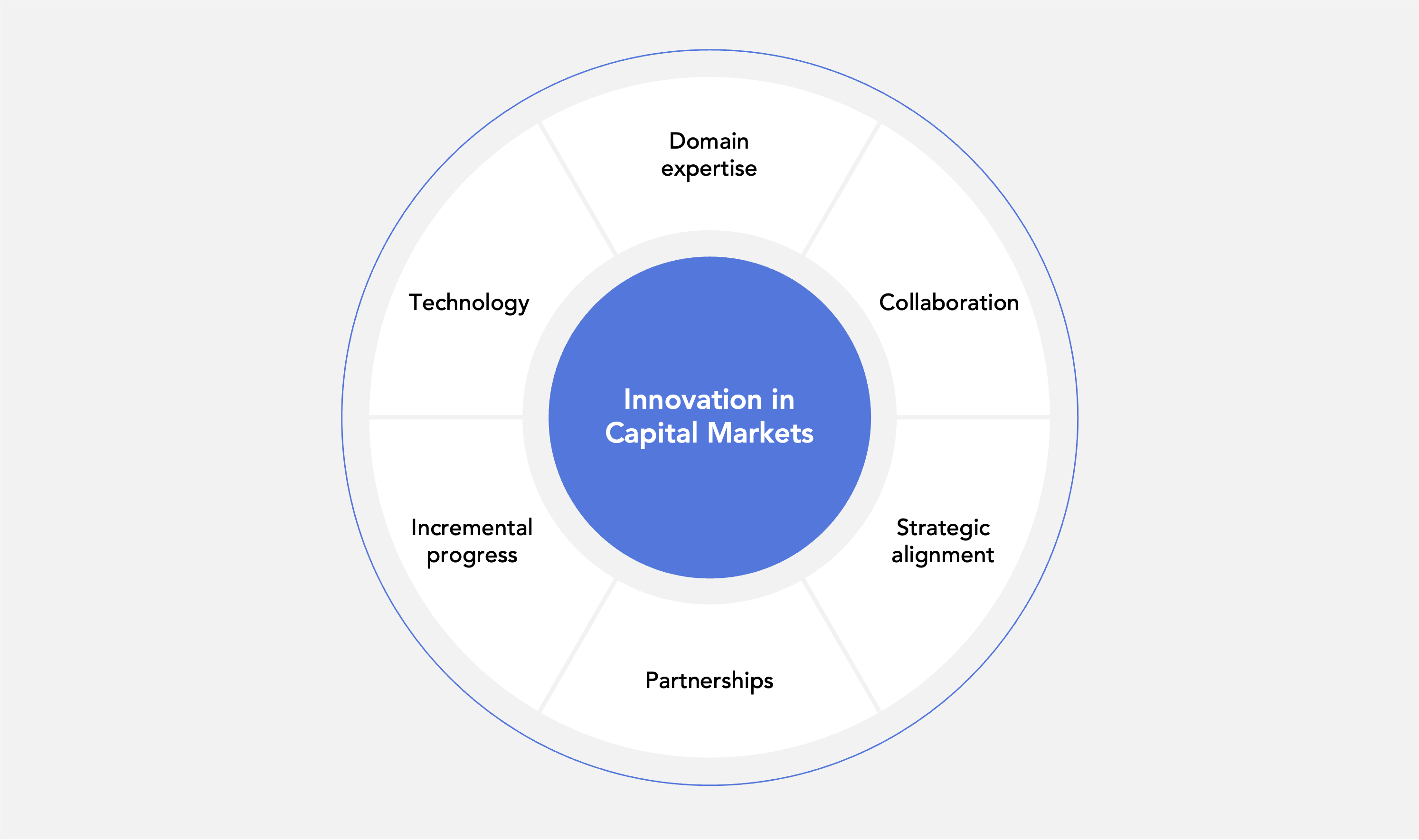

Conclusion: The future of innovation in capital markets

Innovation in capital markets is not just about technology— it’s about having domain expertise, collaboration, strategic alignment, and incremental progress. By leveraging strategic partnerships, innovators can bridge the gap between cutting-edge technology and market complexity. This approach not only reduces risks but also ensures that innovations deliver value early while laying the groundwork for long-term transformation.

The future of capital markets lies in pragmatic, targeted innovation driven by collaboration and a deep understanding of the sector’s unique challenges and opportunities. We’ve identified white spots and continue to look for those founders brave enough to kickstart innovation in one of the most challenging sub segments in financial services technology.

Download the perspective: Challenges and opportunities in capital markets