Agentic finance in commerce: the transition from human-initiated to agent-initiated commerce

Motive Partners invests exclusively in financial services and financial technology. This paper maps a structural shift we are tracking across commerce: the transition from human-initiated to agent-initiated commerce.

FROM CONCEPT TO REALITY

As AI agents become capable of autonomous deci-sion-making and end-to-end execution, commerce infrastructure designed for human-initiated interactions will in-creasingly become a bottleneck. We believe the resulting need for new rails, protocols, and trust layers represents one of the most compelling venture opportunities in fintech today.

The transition from embedded finance to agentic finance is underway, and it’s redefining how commerce is conducted. The strategic implications for fintech entrepreneurs and investors are clear: this is a paradigm shift that rewards those who move early to enable and capitalize on AI-driven transactions. AI systems won’t just recommend products, but also execute transactions end-to-end on a user’s behalf - they will even consider adding ‘pay by instalments’ and choosing the appropriate insurance. Crucially, this doesn’t mean ripping up the rulebook entirely. Although we see startups emerging that are building entirely new payment rails (eg. Skyfire), payment methods (paid.ai) and wallets (Payman) for the agentic age, much of the existing financial infrastructure (payments networks, identity frameworks, compliance regimes) will still be used, but these must be augmented and adapted for a world where software, not humans, initiate actions.

For entrepreneurs, now is the time to build the picks and shovels of agentic finance. That could mean building trust and identity layers (so that “my agent” and “your agent” can transact safely), new protocols and standards (as seen with MCP and open agent platforms), or developer-friendly tools (APIs, SDKs, dashboards) that abstract the complexity of compliance, security, and payment processing for those creating AI agent applications. It also means working closely with incumbents - the Visas, Mastercards, PayPals, Stripes, and Adyens of the world - since they are actively opening up their rails to agent-driven commerce. There is a collaborative opportunity here: startups can bring the agility and fresh approach, while incumbents bring trusted networks and huge customer bases.

GEN I

WHAT IS ALREADY HAPPENING?

At the infrastructure level, networks are rolling out agent-ready credentials and tokenization frameworks (eg Visa’s Intelligent Commerce and Mastercard’s Agent Pay) designed specifically for AI-initiated transactions, while PSPs are releasing developer toolkits (eg Stripe’s and Paypal’s agent toolkits) that allow agents to securely move money, issue virtual cards, and manage post-purchase workflows. While American Express hasn’t launched an agent product yet, its venture arm is active in this space - Amex Ventures and Visa Ventures jointly backed a startup called Nekuda that is building “agentic payments” infrastructure to let users safely delegate payment authority to AI agents within today’s networks. Merchant acquirers like Adyen recently launched their MCP servers, signalling support for open agent-to-agent communication. These early initiatives are bringing the world closer to autonomous, intent-driven commerce.

GETTING STARTED: THE DELEGATED AUTHORITY PARADOX & AI POWERED RISK

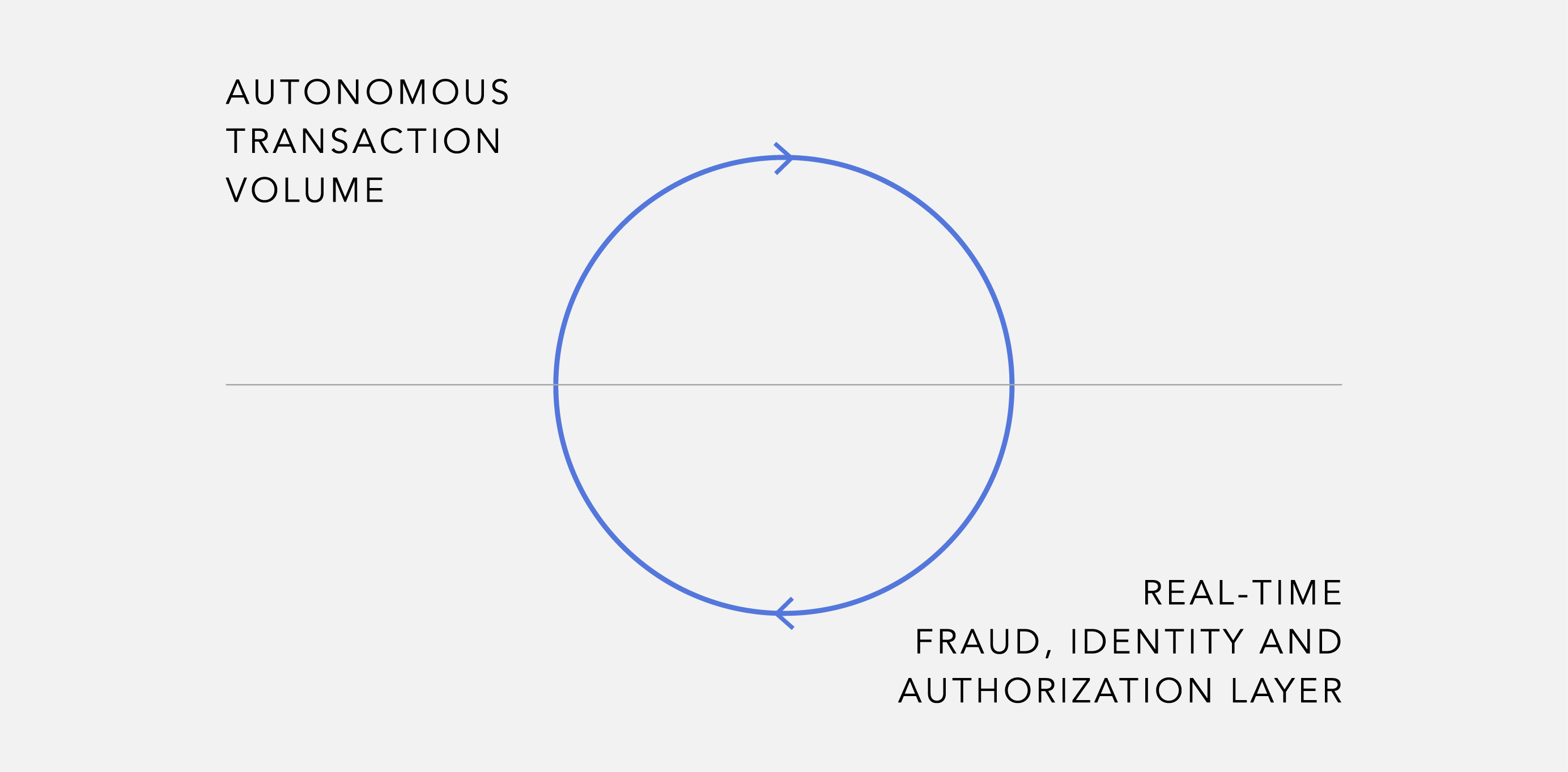

Despite the efforts made at an infrastructure level by incumbents, agentic commerce faces something like a Catch-22 cold start problem: autonomous agents cannot transact at scale without a real-time fraud, identity and authorization layer - but that layer cannot mature without real autonomous transaction volume. The current rollout challenge is therefore not about demand but sequencing.

If payments transaction execution is to change, core risk and security checks and functions must move upstream and occur earlier in the lifecycle of any given transaction. As a result, we see a lot of emerging agentic commerce businesses starting by building a new fraud and risk layer.

Other teams take the approach of training merchants first through simulated agent transaction data. Others again start by focusing on MCP integrations and monetisation, data micro-transactions, in-chat payments - with many trials human:agent as well as agent:agent underway. We believe starting with identity, authorization, and real-time risk detection - and binding them into the earliest stages of an agent’s decisioning workflow - provides the necessary delegated authority foundation upon which payments execution, credit adjudication, and insurance underwriting can reliably be built.

While early intent authentication systems are emerging, what remains unresolved is portable, cross-platform, revocable agent delegation with economic accountability.

Examples: on the identity side, startups like Vouched are issuing ‘Know Your Agent’ digital passports, tackling the portable identity challenge head-on; Microsoft announced Entra ID for AI agents, assigning every Copilot-based agent a unique, revocable identity token with built-in permissions and a kill-switch - a first step toward the kind of cross-platform delegation framework the ecosystem will need.

There is also a growing need for risk engines that operate continuously and instantly, scoring each potential action an agent takes before money moves.

Examples: Oscilar is working on this kind of upstream risk engine - an AI-powered decisioning platform with specialized payment-fraud micro-models that score transactions before an authorization request is even sent, enabling the front-loaded compliance that agent commerce demands; Worldpay recently acquired fraud-detection firm Ravelin, signalling that incumbents too recognize the need to embed real-time fraud intervention directly into agent transaction flows.

WHAT EARLY OPPORTUNITIES EXIST TO INVEST & BUILD?

We see strong opportunities across three key fintech verticals:

- PAYMENTS: AGENT-NATIVE CHECKOUT, CREDENTIALS, AND ROUTING

When an agent can commit funds the moment it finds an in-stock item (without a traditional checkout page), every compliance, identity, and fraud check must be front-loaded to the start of the customer journey. Essentially, the linear flow of browse → add to cart → checkout collapses into a single, pre-authorized action, requiring tokenized credentials, passkeys, and policy controls to get provisioned before the agent ever hits “Pay.”

Examples: this pre-authorized model is already taking shape through experiments like Amazon’s “Buy for Me” agent, which completes purchases on third-party websites using encrypted, pre-provisioned credentials that Amazon itself cannot see - a clear illustration of the tokenized delegation model; Perplexity’s AI answer engine, which integrates with PayPal and Venmo, allowing one-click (or rather, one-prompt) checkout and OpenAI’s Shopify plugin for ChatGPT lets users discover products and complete purchases without ever opening a browser tab. Each of these collapses the traditional checkout funnel into a single intent-driven action. As AI shopping agents proliferate, gift cards / prepaid rails can become a natural payment mechanism for agent-initiated transactions. Players such as our portfolio company finperks are actively building a PSP layer for agent commerce, creating B2B infrastructure for companies building B2C agents and giving them a controlled and secure spending rail. Prepaid rails offer the advantage of built-in guardrails and a simplified checkout experience for agents - no transaction-level authorization required, just entry of a prepaid code, with potential upside through cashback enrichment.

- LENDING: INSTANT, IN-FLOW CREDIT BROKERING AND UNDERWRITING

When an agent is already selecting a product, it can also shop financing options and execute the best one in the same interaction - turning credit into a real-time feature rather than a separate journey.

Examples: Klarna’s shopping assistant integrated into ChatGPT is an early example of credit surfaced at the point of agent interaction; meanwhile, startups like Lendflow are working on bolting AI-driven underwriting engines onto any vertical platform or POS - making real-time credit brokering a composable feature rather than a standalone product.

- INSURANCE: CONTEXTUAL MICRO-POLICIES AND AUTOMATED SERVICING

As an agent books a trip or buys a device, it can fetch a micro-policy quote via API and bundle protection into the same prompt flow - while claims/service automation will make small policies more and more economical over time.

Examples: MarvelX’s ClaimOS uses domain-specific AI to automate claims workflows, aiming to reduce settlement times needed for making embedded micro-insurance more viable; Cover Genius, via its XCover API, already enables contextual micro-insurance for travel, electronics, and events via API - precisely the kind of programmable protection layer that agent workflows can bundle into a single transaction flow.

"Essentially, the linear flow of: browse, add to cart, checkout collapses into a single, pre-authorized action"

GEO OPTIMIZATION & THE EXISTENCE OF BRANDS

In an AI-driven commerce world, discovery will shift from ranking in search results to being selected by an algorithm making Generative Engine Optimization (GEO) the new distribution battleground. Once agents increasingly answer queries and transact directly, “mention share” and machine-readable product data may matter more than traditional marketing. We don’t expect brands to disappear, but their roles will undoubtedly evolve - next to emotional storytelling for humans to trust, performance and credibility signals for agents will become increasingly important.

THE ROAD AHEAD

The commerce experience is moving from one of manual interaction (even if conveniently embedded) to one of delegated intelligence. A shift on par with mobile or cloud. The AI will handle the tedious bits - browsing options, filling forms, comparing offers, managing credentials - leaving humans to simply express intent and enjoy the results. For consumers and businesses, this promises greater convenience and potentially better outcomes (the AI can tirelessly hunt for the best deals or optimal financing).

For the fintech industry, it means a chance to rewrite the playbook on how money moves when “no one” is physically at the controls. The entrepreneurs and investors who grasp the technical mechanics and strategic implications outlined above will be well positioned to build the critical infrastructure of an agentic world. But this Gen 1 landscape - where agents transact for their instructors/principals accessing e-commerce sites - is only the beginning. The real transformation occurs when agentic commerce moves beyond optimizing checkout to fundamentally restructuring who holds bargaining power, how intent is defined, and how value flows between buyers and sellers.

"The commerce experience is moving from one of manual interaction to one of delegated intelligence. A shift on par with mobile or cloud."

Download the perspective. If you’re interested in learning more about Motive Partners, please contact us. Be sure to follow us on LinkedIn for our latest investment news.

Important Information

This paper has been prepared by Motive Partners for informational and educational purposes only. It is not intended to constitute and should not be construed as investment advice, a solicitation, a recommendation, or an offer or invitation to subscribe for or purchase any securities, investment products, or advisory services. The views, analysis, and opinions expressed in this paper reflect the good-faith views of Motive as of the date of publication and are based on information available at that time. They are subject to change without notice and without obligation to update. No representation is made that the information herein is accurate, complete, or current. This paper references certain companies for illustrative purposes. Motive has an existing investment in finperks. All other company references are for illustrative and informational purposes only and do not constitute an endorsement of those companies' products, services, or securities. Forward-looking statements, projections, and opinions regarding market trends and technological developments are inherently uncertain. Actual developments may differ materially from those described. References to market opportunities, venture trends, or investment themes do not constitute a representation that any particular investment strategy will be successful. Nothing herein should be relied upon as the basis for any investment decision. Prospective investors in any Motive Partners fund should rely solely on the applicable fund's offering documents.